5 Fraud Forecasts: What We Got Right and Wrong in 2024 (So Far)

May is knocking on June’s door. And when June opens it, she’ll be welcoming us into the 6th month of the year, about halfway through 2024. Earlier this year, we made some predictions, highlighted emerging trends, and told you some patterns to watch for. Now, as the school year ends and kids are getting their report cards, it’s our turn to grade ourselves. Did we ace fraud analysis? Did we flunk our fraud insights? And what trends are shaping the rest of 2024?

Here’s your industry-level view into the mid-year fraud landscape, our self-assessment of how accurate our predictions have been so far, and what it all means for the rest of 2024.

Industry Analysis #1: Fraud is Outpacing Prevention

Digital transactions continue to rise year-over-year, increasing 90% between 2019 and 2023. And the volume of suspected fraud and scams is riding the same wave: from 2019 to 2023, there was a 105% increase in suspected digital fraud.1

Did we see this coming? Yes.

Granted, hindsight is 20/20, but this fraud rise isn’t surprising to anyone in the industry. Tech innovations are constantly driving fraud innovations, and as the world becomes more digitally savvy it makes sense that fraudsters do as well.

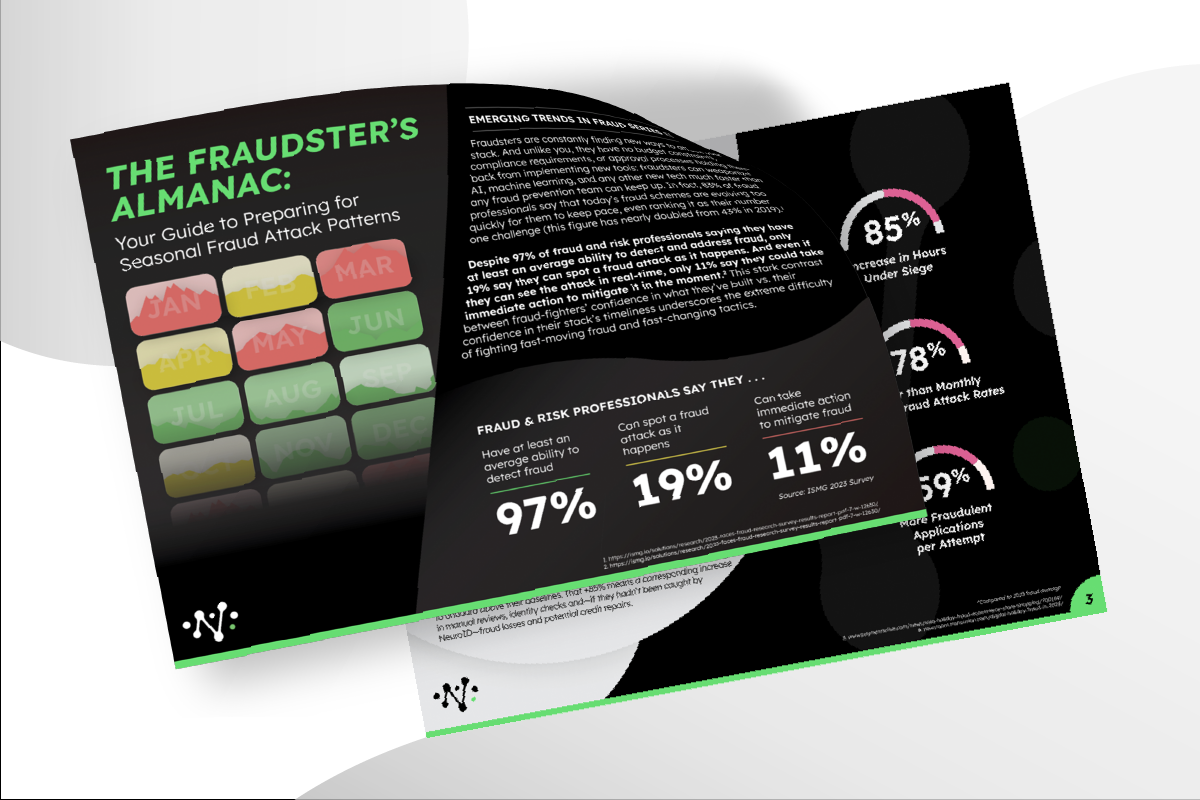

But beyond the normal push-and-pull of fraudsters vs. fraud-fighters, this 105% surge is also driven by the rapid adoption of FedNow, real-time payments (RTP), and other real-time money movement systems (RTMM). With 85% of U.S. consumers asking for real-time payments from businesses, the instant and irreversible nature of RTP/RTMM is also attracting more fraud and scams, posing significant challenges for businesses unprepared to handle real-time fraud detection at scale.2

We’ve long predicted this rise in fraud from RTP/RTMM and have been helping banking and ecommerce industries especially as they balance fraud challenges vs. real-time money opportunities. Businesses unprepared to handle instant fraud detection at scale may quickly be overwhelmed—but we’re here to help. If real-time fraud keeps you up at night, check out our 3 Common Myths About Real-Time Money Movement and Fraud guidebook, which provides actionable steps for anyone hoping to stay competitive with RTMM adoption, without increasing fraud.

Industry Analysis 2: Automation Fraud & The Next-Generation of Bots

Automation fraud, particularly through the use of bots, has surged by 102%.3 Bots are increasingly used for:

- Account creation using stolen identity data: 13.5% of all global digital accounts created in 2023 were fraudulent).4

- Credential stuffing to take over accounts, which saw a 108% year-over-year increase.5

- Carding attacks, where stolen cards are tested, surged by 134% year-over-year.6

- Scraping attacks to steal pricing and other competitive data increased by 107% year-over-year.7

The rapid evolution from Gen 1 to today’s Gen 4 bots has made many traditional fraud protection tools ineffective. If Gen 1 bots were roombas, these Gen 4 bots are Rosey the Robot, the Jetsons’ android maid: hyper-efficient, multi-purpose, and nearly human.

Did we see this coming? Yes.

Because we specialize in bot detection, we’ve noticed changing bot trends and talked to many industry leaders about this shift for awhile. We’ve seen new hybrid bot-human attack strategies take center stage, and how today’s bots, enhanced by AI, can easily bypass previously effective detection tools (sometimes making onboarding easier for bots than for real humans).

We’ve always been and always will be specialists in stopping bot-attacks, no matter the bot generation. NeuroID’s multi-dimensional approach uses behavioral analytics and device/network signals to achieve 99.5% accuracy in bot detection. Coming into the second half of 2024, we’re continuing to innovate to detect ever-more sophisticated bots and help customers stay ahead of this worrisome trend.

Industry Analysis 3: The Rise of Synthetic Identity Fraud (SIF)

Synthetic Identity Fraud (SIF) was already the fastest-growing type of digital fraud, increasing by 6.1% globally from 2022 to 2023 and 184% from 2019 to 2023. This type of fraud, which now comprises 85% of all fraud in the US, involves creating fake identities using real and fabricated information.8

Did we see this coming? Mostly.

NeuroID was built for this very challenge and we’ve been talking about how PII-based detection methods are insufficient against SIF for a decade+. With fraudsters poisoning the well of consumer PII for years, the only surprise is that PII-based fraud mitigation is still a cornerstone of many fraud stacks. Which is not to say its useless . . . but as SIF rises, many of the traditional PII-approaches are unadaptable.

Our behavioral analytics were created to distinguish between data provided from long-term memory versus short-term memory, identifying the behavioral indicators that show if an identity is stolen or synthetic (and if it’s not), without any PII or biometrics collection. We specialize in catching mature or more established synthetics that are able to bypass traditional fraud screens. We expect SIF to continue to rise, and we’ll stay ready for it.

Industry Analysis 4: The Deluge of Deepfakes

Deepfakes aren’t new. But they used to be a small subset of the Dark Web. Then, between 2018 and 2019, deepfake videos rose by 84%.9 Between 2019 and 2020, they rose by 330%.10 And in 2023 alone, deepfake face swap attacks on ID verification systems increased by 704%.11 In just the four years between 2019 and 2023, deepfakes went from niche to a fraud firestorm (and keep in mind, those numbers only count the deepfakes that were detected).

Thanks to advanced machine learning, genAI, cybercriminals, and the vulnerability of less-tech savvy older adults, deepfakes are very effective for fraud. Tools like FraudGPT, which only costs $1700 annually, has put deepfake weapons in the hands of even the most entry-level fraudster.

Did we see this coming? Not at this level.

We’re just seeing the tip of the iceberg in terms of fraudster innovation with new technology. It’s clear they’re targeting biometrics and ID verification specifically as the first easy barriers to overcome, if they haven’t been deepfake-proofed. Which is why a multi-layered, fraud fusion approach that includes behavior is so critical.

At the same time, fraudsters are still making money with less sophisticated schemes. From a fraudsters’ perspective, if it ain’t broke, don’t fix it. Fraudsters won’t increase attack complexity for the same monetization. They work at scale, and efficiency is key. They don’t need to make things more complicated if they can get in with an old-fashioned synthetic identity theft. But the flip-side to that is they will hyperfocus on the laggards who don’t have sophisticated bot prevention and squeeze all the juice they can out of them, so they don’t have to go for the big attacks that take more sophistication. It’s like a cat burglar testing doorknobs. They’re going to go for the house that forgot to lock their front door over the one where they have to break a window, every time.

Industry Analysis 5: Progressive Onboarding

A 2023 study by Baymard Institute showed that complex sign-up processes lead to a 25% abandonment rate. Signicat’s research was even more dire: they found that 6 out of 10 customers abandon the digital onboarding process if it is too long, too complicated, or requires too much information. We’ve been hearing this for awhile as well, from identity verification professionals focused on getting as many customers in the door as possible: if onboarding fraud prevention is too complex, especially with things like one-time-passcodes (OTPs), customers abandon. “Passive” is the word we keep hearing in conversations with customers and thought leaders. Customers and businesses alike want fraud prevention that’s multifaceted, friction-free, and in the background.

Did we see this coming? Yes.

We wrote a whole article about progressive onboarding and fraud a few months ago, and the drumbeat for passive fraud prevention that can act both as a friction-fighter and cost reduction tool has only started beating louder. There’s always ebbs and flows for fraud, and right now, many people we’re talking to are prioritizing customer conversion over combating fraud.

As a passive behavior signal, NeuroID is key to a simpler sign-up approach, where you focus on controls only in the face of potential risk—not at every sign-up step. This is something we’ll be keeping an eye on to evolve more in 2024, especially in the ecommerce space.

6 Months in a Nutshell

The rise in digital transactions and the concurrent wave of increasingly sophisticated fraud techniques, highlights the need for robust fraud detection mechanisms. By leveraging advanced behavioral analytics and device/network intelligence, businesses can better protect themselves and their customers from a wide range of fraudulent activities. As we move into the second half of 2024, whatever trend you’re seeing in your unique fraud state, staying ahead is key. Talk to NeuroID if you want to learn more about a fusion fraud prevention strategy that is future-proof and friction-free.

Footnotes:

- TransUnion State of Omnichannel Fraud 2024 Report

- Discover 5 Payment Trends in Fintech: Emerging Payment Technologies, 2022

- TransUnion State of Omnichannel Fraud 2024 Report

- TransUnion State of Omnichannel Fraud 2024 Report

- Human 2023 Enterprise Bot Fraud Benchmark Report

- Human 2023 Enterprise Bot Fraud Benchmark Report

- Human 2023 Enterprise Bot Fraud Benchmark Report

- Mckinsey Institute Fighting back against synthetic identity fraud 2019

- The evolution of deepfakes: Fighting the next big threat

- Less than 30% of Businesses Have a Plan to Combat Deepfakes

- TransUnion State of Omnichannel Fraud 2024 Report